The gambler’s guide to investing: What is modern portfolio theory?

First National Wealth ManagementJuly 3, 2026

Matt Adamson

Investments Manager

Modern portfolio theory (MPT) is a sophisticated tool to help investors answer two fundamental investment questions:

- What should I invest in?

- How much should I invest?

In this part of our series on gambling and investing, we will dive a little deeper into the foundational concepts of building an investment portfolio.

Our lessons from gamblers — thinking probabilistically, understanding odds, and playing through bad luck — will serve us well here.

However, we will let the investment experts speak for themselves this time around and examine the core of MPT.

What is modern portfolio theory?

One of the benefits of MPT is that it can help us assess those two fundamental questions for any investment, not just traditional assets like stocks and bonds.

While we won’t cover the entire theory, there are three fundamental ideas that are worthwhile for investors to explore.

To keep the examples manageable, our focus will stay on traditional investments such as diversified portfolios of stocks and bonds.

Forming reasonable expectations

Step one of evaluating any investment is forming a reasonable expectation of its future return.

For diversified investments with long performance histories, like stocks and bonds, the historical average is a starting point.

However, investors should be wary of average returns for assets with limited history (less than 50 years) or non-diversified investments, which carry unique risks and can deviate wildly from their averages in the future.

These forecasts are well beyond the scope of the average investor and should be evaluated with extreme caution.

For more traditional investments, we don’t need to stop at historical averages, which can often be improved with price-based forecasts.

For bonds, the starting yield to maturity is very closely related to the future return and is, therefore, a better estimate for investors.

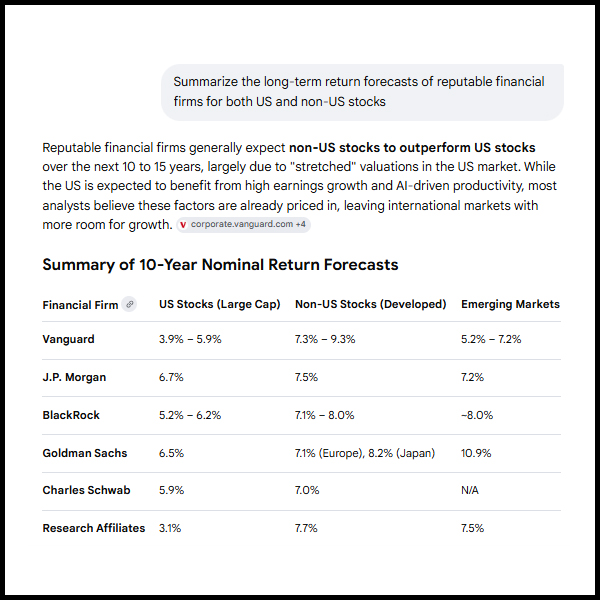

Reasonable forecasting is also available for stocks, but this carries more uncertainty. A good starting point for most investors is the capital markets assumptions of reputable financial institutions, such as the example below.

Investor Takeaway

You must form an expected return for any investment asset in order to compare it to alternatives.

Understanding volatility drag

Once we have reasonable expected returns for our investments, the second step is to account for risk.

There are different ways to assess this, but MPT settles on a statistical concept called variance, often referred to as volatility.

Variance is simply a measure of how much an investment’s actual returns differ from its long-term average.

An investment with high variance, like stocks, might have an average return of 10%, but actual returns are almost never near this number.

In fact, for U.S. stocks, only seven of the last 75 years marked a performance between 8% and 12%, near the long-term average. The other years varied wildly from a high of +45% in 1954 to a low of -38% in 2008.

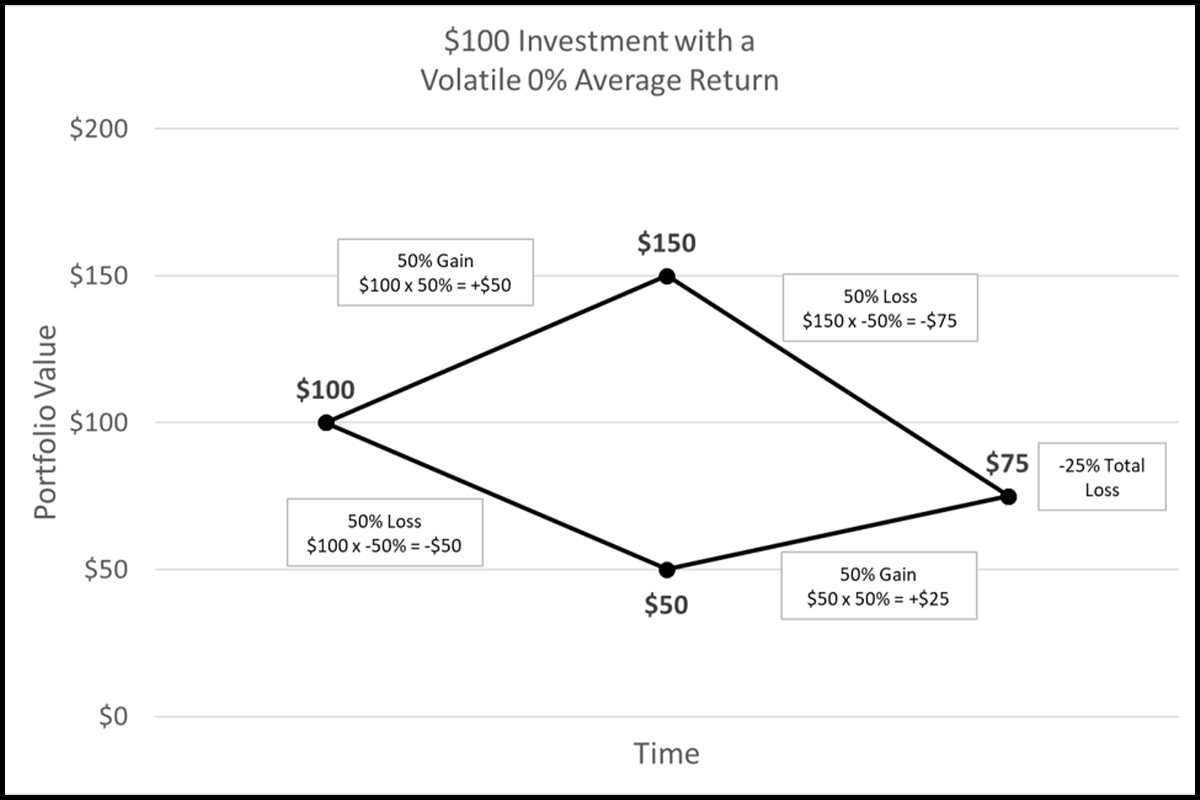

Why should investors care? Because volatility reduces your returns over time.

The classic example here is an investment that either gains 50% or loses 50%. With an average return of 0%, you might expect this to be a wash — but the truth is much worse.

In the most likely scenario, an investor will actually lose 25% on this investment.

Why does this happen? The math of compounding penalizes volatility.

This is one reason why riskier investments should have higher expected returns.

Investor Takeaway

Volatility reduces the return you will earn on an investment, all else equal.

The magic diversifier

Finally, we need to combine our knowledge of expected returns and the negative effect of volatility.

How do these important concepts interact within a real portfolio of investments? The answer is the magic of diversification.

In order to understand it, we need our final idea from MPT: the statistical concept of covariance.

Most investors understand diversification quite well; if I own many different investments, it is likely that at least one of them is doing well, even if others are performing poorly.

For a two-asset portfolio, the gain of one investment may counterbalance the loss of another.

In this case, the volatility of the portfolio is reduced due to the offsetting nature of the two asset returns. As we know, this has a beneficial effect on the compounding of returns.

In this example, because one investment goes up when the other goes down, the two assets would usually have a negative covariance*.

Assets with low or negative covariance are beneficial to a portfolio because they decrease portfolio volatility and maximize diversification benefits.

Investor Takeaway

Low or negative covariance assets improve the risk/return profile of a portfolio through the benefits of diversification.

Applying modern portfolio theory to your investments

In summary, modern portfolio theory combines our knowledge of expected returns, volatility, and covariance to help evaluate new and existing investments in the context of a broader portfolio.

While the math of doing so is beyond this short blog post, investors can benefit from an understanding of how these three concepts work together.

I would be happy to answer any questions you have about modern portfolio theory and how it applies to your investments; simply reach out!

*This is a sloppy description since covariance measures the joint deviation of two investment returns from their average return, not whether returns are positive or negative. However, the benefit is very easy to see in this case. Said correctly, if two investments have negative covariance with each other, one would tend to outperform its average when the other was underperforming its average. This could happen even if both investments have a positive return.

Investment experts

We will work with you to create an investment plan that makes sense and can be adjusted when life happens.

I'm Interested